On March 28, 2026, AgiBot’s co-founder Peng Zhihui announced a milestone that would reshape the industry’s understanding of what was possible: AgiBot’s 10,000th general-purpose embodied robot, the Expedition A3, had officially rolled off the production line. In just 15 months, AgiBot had scaled production from 1,000 to 10,000 units—a tenfold increase. The acceleration was equally remarkable: it took the company 11 months to go from 1,000 to 5,000 units, but only three months to add another 5,000—a fourfold increase in production velocity.

For AgiBot, founded only three years ago, the journey from concept to mass production has been compressed into a timeframe that would have seemed impossible just a few years earlier. The company’s revenue trajectory tells a similar story: it surpassed 1 billion yuan (approximately US$140 million) in its third year of operation, and now aims to reach 10 billion yuan by its fifth year. The company has set a 2026 target of producing tens of thousands of robots annually.

The significance extends far beyond one company’s production metrics. AgiBot’s journey from 1,000 to 10,000 units in 15 months is a microcosm of an industry-wide transformation that has taken place in just three years. In 2023, China had roughly 20 companies that had publicly released humanoid robot products. By 2025, that number had exploded to over 140 manufacturers, with more than 330 distinct humanoid robot models unveiled.

I. The XYZ Curve: A Roadmap for the Industry

AgiBot’s chairman and CEO Deng Taihua has articulated a framework for understanding the industry’s evolution that has become widely cited. Known as the “XYZ Development Curve,” it maps the trajectory of embodied intelligence across three phases:

- X Curve (2022–2025): The “Development and Trial Period.” During this phase, the industry completed the critical transition from prototypes to scaled production. Companies moved from laboratory concepts to manufacturing reality, establishing the foundational capabilities needed for commercialization.

- Y Curve (2026–2030): The “Deployment and Growth Period.” This is where the industry now finds itself. The focus shifts to improving hardware consistency, scaling delivery capabilities, and simultaneously advancing interactive intelligence and operational intelligence. The challenge is no longer whether robots can be built, but whether they can be deployed reliably at scale.

- Z Curve (2030 and beyond): The “Deployment and Popularization Period.” In this phase, embodied intelligence is expected to unlock productivity across key sectors including manufacturing, logistics, and services. The goal is to move from early adopters to mainstream deployment.

Deng has declared 2026 the first year of the “deployment state” for embodied intelligence—the moment when the industry formally transitions from “development mode” to “deployment mode,” from “being able to move” to “being able to work.”

Unitree Robotics: The Four-Legged Juggernaut Expands

While AgiBot captured headlines in humanoid robotics, Unitree has been quietly building a dual-platform empire. In February 2026, Unitree unveiled its latest four-legged robot, the Unitree As2. The specifications are striking: weighing just 18 kilograms, it can support a 105-kilogram adult standing on its back. It delivers 90 N·m of peak torque—approximately twice the power of its predecessor—with a no-load battery life exceeding four hours and a top speed of 5 meters per second. The As2 features IP54 weather resistance, allowing it to operate in rain and shallow water, and is powered by a bionic embodied large model for smooth, low-latency motion.

Unitree has also made significant strides in humanoid robotics. The company has filed for an IPO on Shanghai’s STAR Market and continues to expand its global footprint. Unitree’s ability to cross-subsidize its humanoid development with its established four-legged robot business has given it a unique financial runway.

Fourier Intelligence: The Medical Rehabilitation Specialist

Fourier Intelligence has carved out a differentiated path—focusing on medical rehabilitation. The company’s GR-2 general-purpose humanoid robot has entered production lines at SAIC-GM, handling parts sorting, with a planned delivery of 100 units in 2026 priced at US$180,000 each. Simultaneously, the GR series is achieving routine deployment in medical rehabilitation settings.

Fourier’s origins lie in professional rehabilitation robotics. The company has developed multiple devices targeting different functional impairments, including the ArmMotus EMU 3D upper-limb rehabilitation robot and the ExoMotus M4 lower-limb exoskeleton for gait training. These devices laid the hardware foundation for the company’s rehabilitation expertise.

The company’s self-developed FSA actuators have achieved a threefold increase in torque density, supporting both remote operation and autonomous mode switching, with an open SDK for secondary development. Fourier’s core advantage lies in years of accumulated medical robotics technology, building a hardware-software integrated, active-interaction technology platform covering full-stack capabilities from core components to complete machines.

Fourier has also pushed into the frontier of brain-computer interface technology. The company has invested in the brain-computer interface company Gestalt, with the goal of developing a closed-loop training mechanism that connects “intention—execution—perception feedback.” This approach aims to address the fundamental challenge faced by severe rehabilitation patients: the disruption of the “central command—peripheral execution—sensory feedback” neural loop.

Xiaomi CyberOne: From Laboratory to Factory Floor

Xiaomi has also made significant strides in 2026. In March, the company’s humanoid robot left the laboratory and entered the Xiaomi automotive factory for real-world testing. At a self-tapping screw insertion station in the die-casting workshop, the robot achieved three hours of continuous autonomous operation without human intervention, with a bilateral installation success rate of 90.2% and a single-process cycle time of 76 seconds—fully compatible with the factory’s 76-second production line rhythm.

Galaxy General: The Embodied Large Model Leader

Galaxy General has emerged as one of the fastest-rising companies in the 2026 humanoid robotics landscape. Between January and March 2026, the company completed financing rounds totaling at least 1 billion yuan, achieving a valuation exceeding US$3 billion. The company’s technology stack is fully self-controlled, covering three critical areas: complete machine motion control, embodied AI large model integration, and dexterous manipulation.

Leju Robotics: The Mass Production Line Pioneer

Leju has taken an early lead in production capacity. On March 30, the company and Dongfang Precision jointly launched China’s first 10,000-unit-level humanoid robot automated production line in Guangdong, capable of producing one humanoid robot every 30 minutes with an annual capacity exceeding 10,000 units. In April 2026, Leju’s Shenzhen Longhua pilot production line also went into operation, leveraging the industrial chain synergy advantages of the Guangdong-Hong Kong-Macao Greater Bay Area.

Other Emerging Contenders

Beyond the companies already highlighted, a wave of additional players has achieved notable milestones:

- Xingdong Era, incubated by Tsinghua University, completed financing rounds totaling at least 1 billion yuan between January and March 2026, joining the ranks of embodied intelligence leaders with full-stack self-developed capabilities covering core components.

- Zhongqing Robotics has carved out a unique position: its PM01 robot has been selected as a candidate for China’s first humanoid robot astronaut, preparing to participate in space exploration missions. The company has also achieved dynamic performances including dance and combat demonstrations.

- AI² Robotics has been ranked first in industry rankings, pioneering VLA (Vision-Language-Action) technology. The company developed the world’s first full-body embodied large model, GOVLA, enabling unified output of full-body control logic and movement trajectories, granting robots 360-degree environmental perception and whole-body coordination across 34 degrees of freedom.

- Kepler Robotics focuses on the “industrial blue-collar robot” positioning, targeting automotive manufacturing applications.

- Magic Atom secured a 150 million yuan robot procurement order in the health and wellness sector in April 2026, setting a record for single-order size in that category and marking its commercial deployment volume’s entry into the first tier.

- DeepRobotics leads globally in four-legged robotics, with Hangzhou accounting for over 80% of China’s four-legged robot market share. The company is now positioning for expansion into the humanoid robotics track.

- Independent Variable Robotics completed a nearly 2 billion yuan Series B financing round in April 2026, led by Xiaomi Strategic Investment and HSG, joining the ranks of ten-billion-yuan valuation companies.

- Zhuoyide Robotics unveiled the world’s first fully bionic embodied intelligent robot, the “Moya” series, at the Shanghai International Logistics Festival, featuring bionic dexterous hands capable of fine grasping and flexible interaction.

- Data Robotics, with its Ginger series as one of China’s earliest humanoid robot products, continues to explore commercialization paths.

- SIASUN, as a state-owned benchmark for China’s robotics industry innovation, showed its latest humanoid robot achievements.

- Tiangong Robotics, as a Beijing E-Town local robotics enterprise, benefits from Beijing’s 100 billion yuan government investment fund ecosystem.

Key Emerging Forces

- Xinghai Tu became a ten-billion-yuan unicorn in just two years, with a top-tier algorithm team leading foundational model development.

- Qianxun AI has achieved zero-defect mass production in new energy manufacturing lines, with its “Xiaomo” robot serving the world’s first humanoid robot power battery PACK production line in partnership with CATL, maintaining operational accuracy above 99.5%.

- Songyan Power is advancing the light-weight, low-cost path to bring humanoid robots into consumer scenarios, appearing alongside other Chinese humanoid robotics companies on the 2026 CCTV Spring Festival Gala.

III. The Numbers Behind the Transformation

The rapid emergence of China’s humanoid robotics industry is reflected in its market metrics.

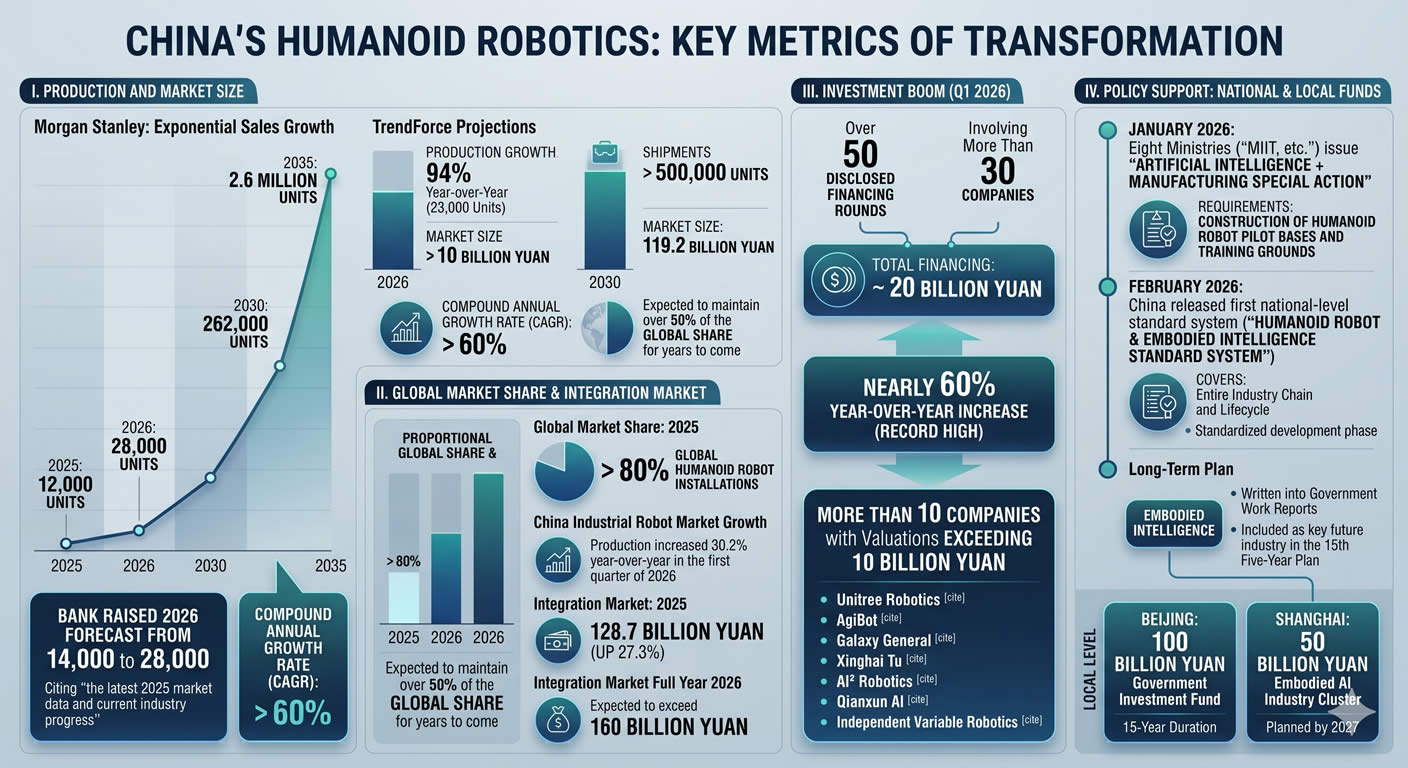

Production and Market Size. According to Morgan Stanley, China’s humanoid robot sales are projected to grow exponentially: from approximately 12,000 units in 2025 to 28,000 units in 2026, reaching 262,000 units by 2030 and 2.6 million units by 2035. The bank raised its 2026 forecast from 14,000 to 28,000 units, citing “the latest 2025 market data and current industry progress.”

Industry research firm TrendForce projects China’s humanoid robot production will grow 94% year-over-year in 2026 to 23,000 units, with the market size exceeding 10 billion yuan. By 2030, shipments are expected to surpass 500,000 units, with the market projected to reach 119.2 billion yuan, representing a compound annual growth rate exceeding 60%. China’s humanoid robot shipments are expected to maintain over 50% of the global share for years to come.

Global Market Share. In 2025, China already accounted for over 80% of global humanoid robot installations. The country’s industrial robot market has also shown robust growth: industrial robot production increased 33.2% year-over-year in the first quarter of 2026. China’s industrial robot integration market reached 128.7 billion yuan in 2025, up 27.3%, and is expected to exceed 160 billion yuan for the full year 2026.

Investment Boom. The capital markets have taken notice. In the first quarter of 2026 alone, China’s embodied intelligence sector saw over 50 disclosed financing rounds involving more than 30 companies, with total financing of approximately 20 billion yuan—a nearly 60% year-over-year increase and a record high. More than ten companies have now achieved valuations exceeding 10 billion yuan, including Unitree Robotics, AgiBot, Galaxy General, Xinghai Tu, AI² Robotics, Qianxun AI, and Independent Variable Robotics.

Policy Support. The Chinese government has provided consistent, high-level support for the industry. In January 2026, eight ministries including the Ministry of Industry and Information Technology jointly issued the “Artificial Intelligence + Manufacturing” Special Action Implementation Opinion, requiring the construction of humanoid robot pilot bases and training grounds. In February 2026, China released its first national-level humanoid robot and embodied intelligence standard system covering the entire industry chain and lifecycle, marking the industry’s entry into a standardized development phase. Embodied intelligence has also been written into government work reports and included as a key future industry in the 15th Five-Year Plan.

Local governments have matched this ambition with resources. Beijing has established a 100 billion yuan government investment fund with a 15-year duration. Shanghai has released a plan to build a 50 billion yuan embodied AI industry cluster by 2027.